The United States as a Developing Country*

Reversion, Regression, Compensation

It’s much worse than I thought. The savage world conjured in Lionel Shriver’s novel of 2015, The Mandibles, which tells the story of an America that has reneged on its national debt and reverted to barbarism, now looks like realist fiction. For the new dimension on the horizon of investors’ expectations is default. But wait, isn’t that what happens in what was once called the “third world,” then “developing countries,” now “emerging markets”? Can Trump actually take us back to the 19th century, when the United States was, in fact, a developing country?

Well, yes, he can.

I wrote on Thursday that it was the bond market, not the stock market, that caused Trump to reverse course and “pause” the tariff binge he was on, having been enabled by his ignorance, emboldened by the compliance of Congress, but stymied by the sell-off of US Treasuries, both real and threatened. Now it looks as though his stupid, reckless campaign may have done irreparable damage to the standing of those bonds as a reliable long-term investment, which until this week were the safe haven of investors worldwide, especially in times of crisis, because they are guaranteed by the full faith and credit of the United States government.

That guarantee was never in question, not even when civil war divided the country into warring armies. But when the US government looks capable of destroying itself and dragging the world’s economy down with it, all bets are off, including the bets made on its ability—or, in this case, its willingness—to pay its debts. For the question investors now have to ask is, has Trump put the US on the road to default, where the only off ramp is a declaration of national bankruptcy? That would of course be in character for him, a move to be expected from a failed businessman who takes everything personally, even the leadership of the most powerful nation on earth. But is that where the rest of us are now headed?

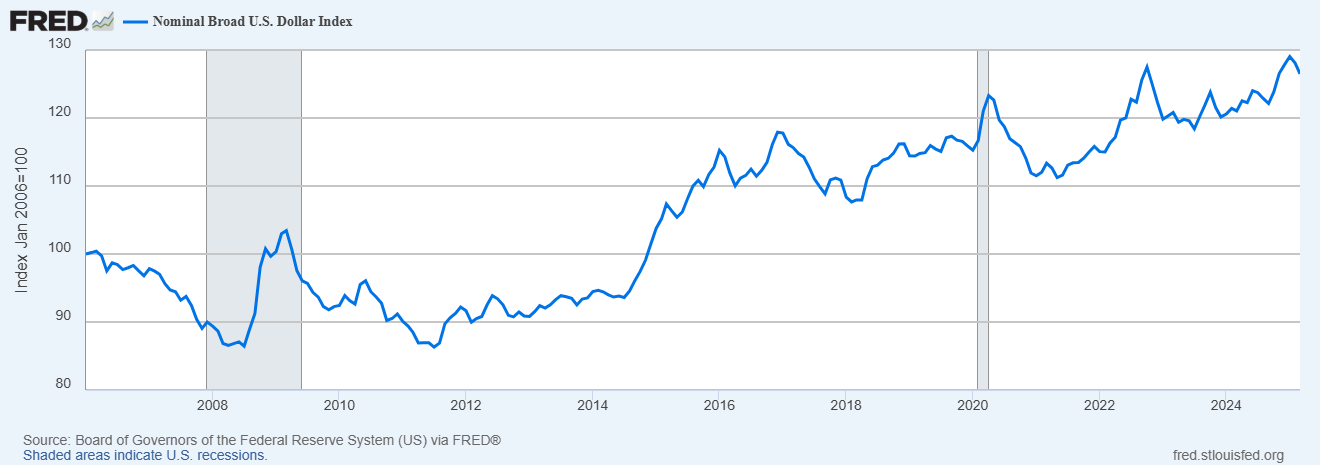

The generous reading of his tariff policy holds that the long-term goal is to reduce trade deficits by devaluing the dollar—just not to the point where investors “diversify away” from it in search of another, more reliable reserve currency. That is the core argument of Stephen Miran’s widely cited paper on the so-called Mar-a-Lago Accord (he is now the head of Trump’s Council of Economic Advisers). The assumption here has been that investors don’t really have a choice, because neither the Chinese yuan nor the EU’s Euro is ready to play the role that the dollar has since World War II: these relatively new currencies are used in a substantial proportion of international trade, but can’t yet cover the existing or the prospective scale of global transactions.

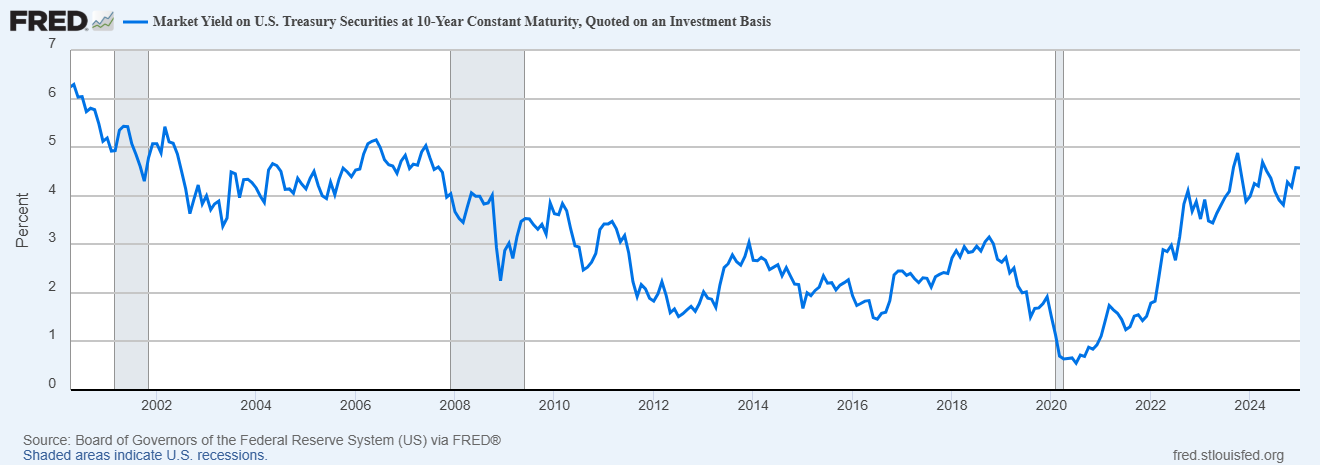

Now it seems that investors are testing that assumption. The dollar has declined precipitously against other currencies, but bond prices have meanwhile risen because demand for both has fallen. Trump has had his way with the dollar, in other words, but the devaluation has been much greater than anyone expected. But if the dollar’s value declines along with the government’s capacity to pay a national debt that metastasizes because its revenues have been slashed by tax cuts, diminished trade, increased unemployment, plus inflation—another full-blown economic crisis—will the market in US Treasuries crash? What then?

I leave you with a summary of where we stand by Noah Smith, an economist who draws on Bloomberg to suggest that a very real possibility is wholesale capital flight from the US, as if this nation is indeed a “banana republic,” or has in fact reverted to its former status as a developing country.

“Usually, when economic times are bad, people rush to buy Treasuries instead of selling them. Even in the financial crisis of 2008, when it was the U.S. economy that was crashing, investors all over the world rushed to move their money into America, because Treasuries were considered the safest asset in the world. So yields went down, and the dollar went up:

“Such was the awesome power of America’s reputation for safety and stability that even an American economic crisis caused people to flee to the safety of U.S. government bonds.

“That’s not happening this time, though. This time, investors are responding to a U.S. economic crisis by looking around for the exits. The most likely reason is that investors have begun to see U.S. government bonds as a risky asset instead of a safe one. And the obvious reason is Donald Trump’s economic policies. Bloomberg explains:

Billed on Wall Street as so rock-solid safe they’re risk-free, US Treasury bonds have long served as first port of call for investors during times of panic . . .But now, as President Donald Trump unleashes an all-out assault on global trade, their status as the world’s safe haven is increasingly coming into question . . .

[In recent days,] investors have often dumped 10- and 30-year Treasuries— pushing prices down and yields up—at the very same time they frantically sold stocks, crypto and other risky assets . . . .They are trading, in other words, a little like a risky asset themselves. Or, as former Treasury Secretary Lawrence Summers says, like the debt of an emerging-market country . . . .

Investor confidence in US bonds can no longer be taken for granted. . . . Treasuries and the dollar get their strength from “the world’s perception of the competence of American fiscal and monetary management and the solidity of American political and financial institutions,” said Jim Grant, founder of Grant’s Interest Rate Observer, a widely followed financial newsletter. “Possibly, the world is reconsidering.“ . . . Treasuries are not behaving as a safe haven,” said ING rates strategist Padhraic Garvey. . . . “The here and now is painting Treasuries as a tainted product, and that’s not comfortable territory.”

“

**This the title of a 1992 essay collection by Martin J. Sklar, a brilliant historian who used it to depict the unfinished character and unfulfilled promise of his beloved country. Toward the end of his life, he gave up on that promise, and joined the reactionary forces that would one day deliver this nation unto the careless hands of the current president. I wish he were still here, so he could laugh with me at how Trump has drained his book title of all irony.